If you win a lottery of million dollar, how would you like your payout? Lump sum or annuity payment? If you choose lump sum, you will receive smaller immediate payout, but choosing an annuity spreads payments over several years, and the overall amount is generally higher than the immediate payout. Despite higher payment, more than 90% of lottery winners choose lump sum over annuity payment1. Why? Because the sum of money available today worth more than the same amount in the future. This is an important financial concept called the Time Value of Money (TVM). This principle, also known as the present discounted value, underlies the idea that because money can earn interest or returns, any amount of money is worth more if received sooner, and a delay in investment represents a lost opportunity.

TVM is a core principle of finance, and here are few key reasons to learn about it.

Optimizing Investments: TVM helps in evaluating the potential growth of investments over time, allowing individuals and businesses to compare different financial options and choose the most lucrative one. By recognizing that a dollar today is worth more than a dollar tomorrow, investors can maximize their returns and build wealth more effectively.

Effective Loan Management: Knowledge of TVM is essential in understanding the real cost of loans and mortgages. It helps borrowers comprehend the impact of interest rates and repayment schedules, enabling them to make better decisions and manage debt more efficiently.

Planning for the Future: TVM is indispensable in retirement planning and setting long-term financial goals. It allows individuals to determine how much they need to save and invest today to achieve their desired financial outcomes in the future. This foresight ensures financial security and peace of mind. See the retirement calculation below.

Valuation of Financial Assets: Accurately valuing stocks, bonds, and other financial instruments requires a deep understanding of TVM. It enables investors to calculate the present value of future cash flows, facilitating more accurate assessments of an asset's worth and better investment choices.

Making Informed Decisions: Whether deciding between a lump sum payment or annuity, assessing investment opportunities, or planning for major life expenses, TVM provides the analytical framework needed to make sound financial decisions. It empowers individuals to weigh the benefits and risks associated with different financial scenarios.

Let's illustrate the Time Value of Money with a practical example.

Suppose you have the option to receive $10,000 today or $10,000 five years from now. Which choice will be best for you? To make an informed decision, let’s consider the time value of money. Assume you can invest money at an annual interest rate of 6% what would be the future value.

The formula for future value is:

where:

PV is the present value ($10,000),

r is the annual interest rate (6% or 0.06),

n is the number of periods (5 years).

Substituting the values:

FV=10,000×(1+0.06)5

FV≈ $13,382.00

So, $10,000 today will grow to approximately $13,382 in five years if invested at 6% annually.

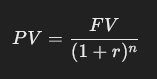

Now, let's calculate the present value of $10,000 received five years from now, discounted at an annual interest rate of 6%.

The formula for present value is:

Substituting the values:

PV=10,000/(1+0.06)5

PV≈ $7,462.00

So, $10,000 received five years from now is worth approximately $7,462.00 today, when discounted at 6% annually.

In this hypotgetical situation, if you receive $10,000 five years from now, in today’s term it will worth only $7,462 but if you receive $10,000 today it can grow to $13,382 in five years considering 6% of discounted or interest rate respectively.

Retirement Planning Calculations

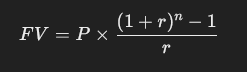

We can also use TMV to calculate how much do we need to start save to reach our retirement nest egg goal. Suppose you are 30 years old and just started your career. You want to have 2 million dollars in your retirement account by the time you retire at age 65. After doing your homework, you found that you can get an average of 6% return in your investment. So, how much money do you need to start saving every year or month?

The formula to calculate the annual savings (PP) needed to achieve a future value (FV) is:

Where:

FV is the future value you want to achieve ($2,000,000).

r is the annual interest rate (6% or 0.06).

n is the number of years you will be saving (65 - 30 = 35 years).

P is the annual savings amount you need to find.

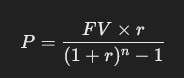

Rearranging the formula to solve for P:

*The subtraction of 1 in the formula (1+r)n−1 accounts for the geometric progression of the compounding effect of each individual payment. It ensures that the future value accurately reflects the sum of all the payments compounded at the given interest rate over the specified period. Without subtracting 1, the formula would not correctly calculate the series sum, leading to an incorrect future value.

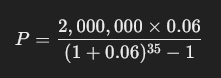

Let’s plug the values in

P » $17,950.98/year

You need to save approximately $17,950.98 each year or (approx. $1,495 per month) to retire with $2 million at age 65, assuming a 6% annual interest rate.

Plug in your age, your retirement egg nest target, and your desired growth rate in the given formula to find out how much you need to start saving each year.

TVM and Inflation

TVM and inflation are closely related financial concepts. Both factors need to equally given attention while investing. Inflation reduces the purchasing power of money over time. This means that the money you have today will not buy as much in the future due to the rising prices of goods and services. As a result, the value of future cash flows is diminished when adjusted for inflation. For example, if an investment yields a nominal return (not adjusted for inflation) of 6% and inflation is 2%, the real return (adjusted for inflation) is approximately 4%. Therefore, inflation must be considered to understand the true value of future returns.

Conclusion:

The Time Value of Money is a cornerstone of financial literacy and a fundamental principle that underpins all areas of finance and investment. There is hardly any area of finance, whether it is your personal finance or small or large business where the financial decision will not be influenced by the TVM. Hence, understanding TVM is crucial for anyone looking to make informed financial decisions. It is also important for valuing financial assets, comparing financial options, and making strategic financial decisions. TVM enables individuals to harness the power of compounding to grow wealth and achieve financial security. Mastering TVM principles leads to better financial planning, smarter investment choices, and long-term financial success. The bottom line is, the future value of money never be equal to present-day dollars. Warren Buffett once said, "Time is the friend of the wonderful company, the enemy of the mediocre."

Gajendra Shrestha

Financial Professional

Herriman, Utah